Allocating capital to a private real estate fund is not a passive decision — it is a capital allocation decision. While investors may not be involved in day-to-day operations, the diligence required before committing capital should mirror the rigor applied by institutional investment committees.

In today’s U.S. environment — characterized by elevated interest rates, constrained debt markets, and disciplined underwriting — capital preservation and execution capability matter more than headline return projections.

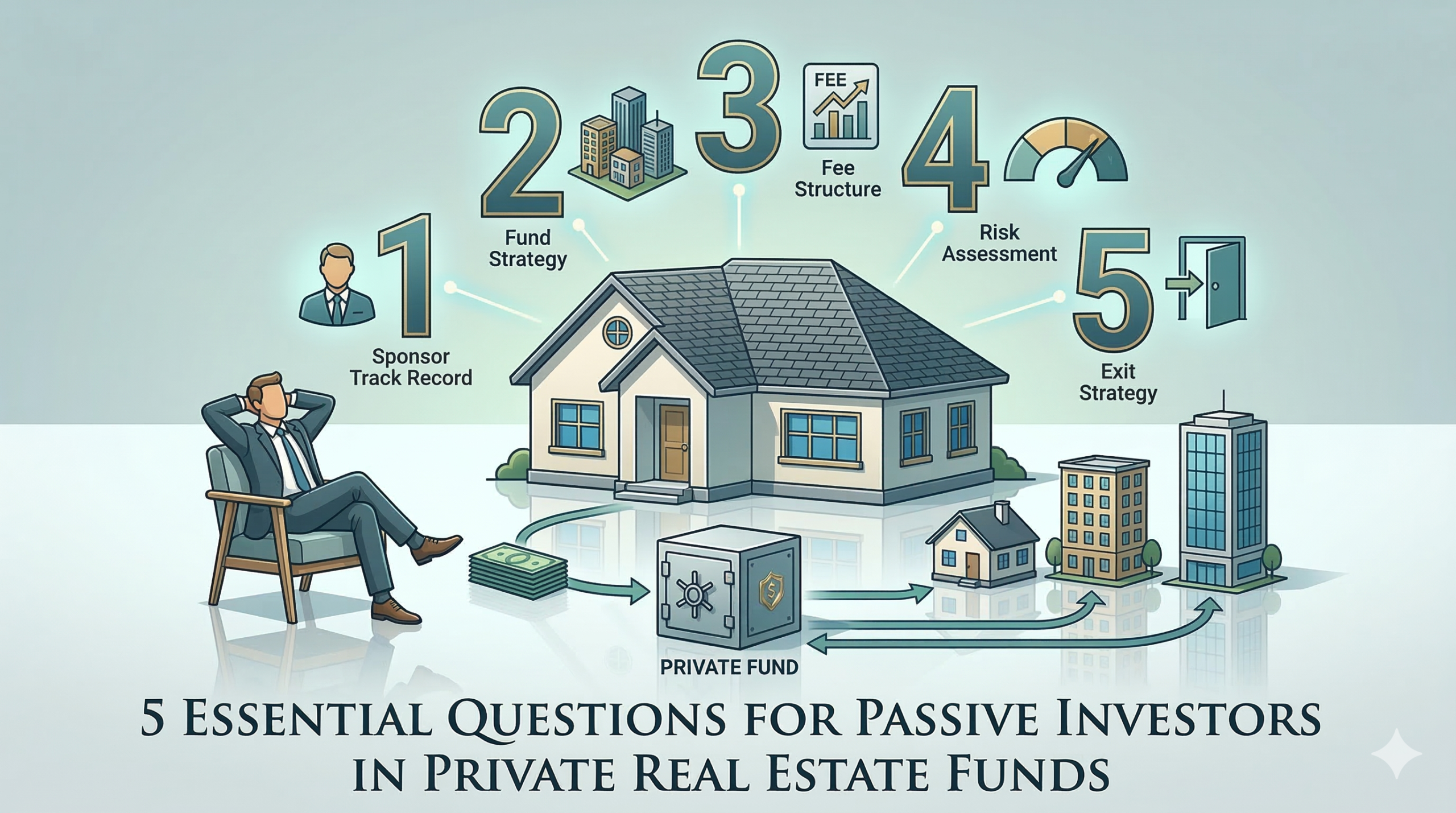

Before committing capital to a private multifamily real estate fund, passive investors should evaluate five core areas: strategy, market exposure, underwriting discipline, capital structure, and sponsor capability.

Every fund operates within a defined risk-return spectrum: core, core-plus, value-add, or opportunistic.

Understanding the strategy clarifies expected volatility, hold period, and return expectations.

Passive investors should ask:

A fund lacking strategic clarity introduces execution drift risk.

Market exposure drives structural performance.

Investors should request analysis on:

Funds targeting structurally strong secondary and tertiary markets often benefit from demographic tailwinds without excessive entry pricing pressure seen in primary metros.

Passive investors should be cautious of funds allocating capital into markets experiencing supply saturation or declining net migration.

Underwriting discipline defines downside resilience.

Key questions include:

Optimistic revenue projections without market validation represent projection risk rather than investable return.

Investors should examine:

Expense underestimation is one of the most common drivers of NOI erosion.

Exit valuation materially impacts projected IRR.

Investors should ask:

Funds that rely on cap rate compression to meet return targets introduce speculative exposure.

Leverage magnifies both gains and losses.

Passive investors should understand:

Conservative leverage improves refinance flexibility and reduces forced sale risk.

In today’s capital markets environment, funds emphasizing moderate leverage and balance sheet durability often demonstrate superior long-term resilience.

Sponsor capability is the primary determinant of execution risk.

Investors should request:

Consistency across cycles signals operational maturity.

Key infrastructure considerations include:

Vertically integrated platforms often exhibit tighter cost control and faster operational response.

Alignment reduces agency risk.

Investors should evaluate:

Sponsors with meaningful capital invested alongside LPs demonstrate confidence and alignment.

Fee structures should reward performance, not simply asset accumulation.

Return realization depends on credible exit pathways.

Funds with flexible exit strategies reduce exposure to unfavorable capital market windows.

Transparency signals operational discipline.

Passive investors should confirm:

Robust reporting frameworks reflect institutional standards.

Passive investors should compare projected returns relative to risk exposure.

A lower projected return with durable cash flow and conservative leverage may be preferable to a higher-risk structure dependent on optimistic assumptions.

Sponsor capability and underwriting discipline are often the most critical determinants of long-term performance.

Moderate leverage that maintains strong debt service coverage ratios is generally viewed as prudent under current interest rate conditions.

Because exit valuation sensitivity can materially impact projected returns. Conservative exit assumptions reduce speculative exposure.

Institutional frameworks prioritize risk-adjusted returns and durable cash flow over maximizing projected IRR.

Passive investing in a private real estate fund requires active diligence. Institutional-level evaluation — across strategy clarity, market fundamentals, underwriting rigor, leverage discipline, sponsor capability, and alignment — materially reduces risk exposure.

In today’s U.S. multifamily market, disciplined capital allocation separates durable long-term compounding from speculative exposure. Passive investors who adopt an institutional evaluation framework improve both capital preservation and performance consistency.